Before the coronavirus pandemic hit last March, Danny Samet, 28, had big financial plans for the year.

The freelance tour manager and merchandiser for bands had a goal to pay off his credit card debt, which is about $6,000, he said. Once he'd done that he was considering looking to buy a house in Cincinnati, where he lives when he's not on the road.

Now, everything has changed.

The music industry closed due to the pandemic, leaving Samet, also a volunteer for Be An #ArtsHero, out of work. While he was able to stay afloat with savings, pandemic unemployment assistance and gigs including working the Georgia election, he's had to put all other financial plans on hold.

Get New England news, weather forecasts and entertainment stories to your inbox. Sign up for NECN newsletters.

"I have just been treading water with it," Samet said. "I've just kind of been floating and just getting by day to day."

Samet is like many other young adults that have had to delay financial milestones because of the coronavirus pandemic. As many as 57% of those aged 18 to 40 – Generation Z and millennials– said that they'd put off a major milestone due to the coronavirus pandemic, according to an online March survey of 2,442 adults from Bankrate.

Older Americans seem to have fared better amid the pandemic – only 26% of those over 40 said they'd delayed a milestone in the last year, according to the survey.

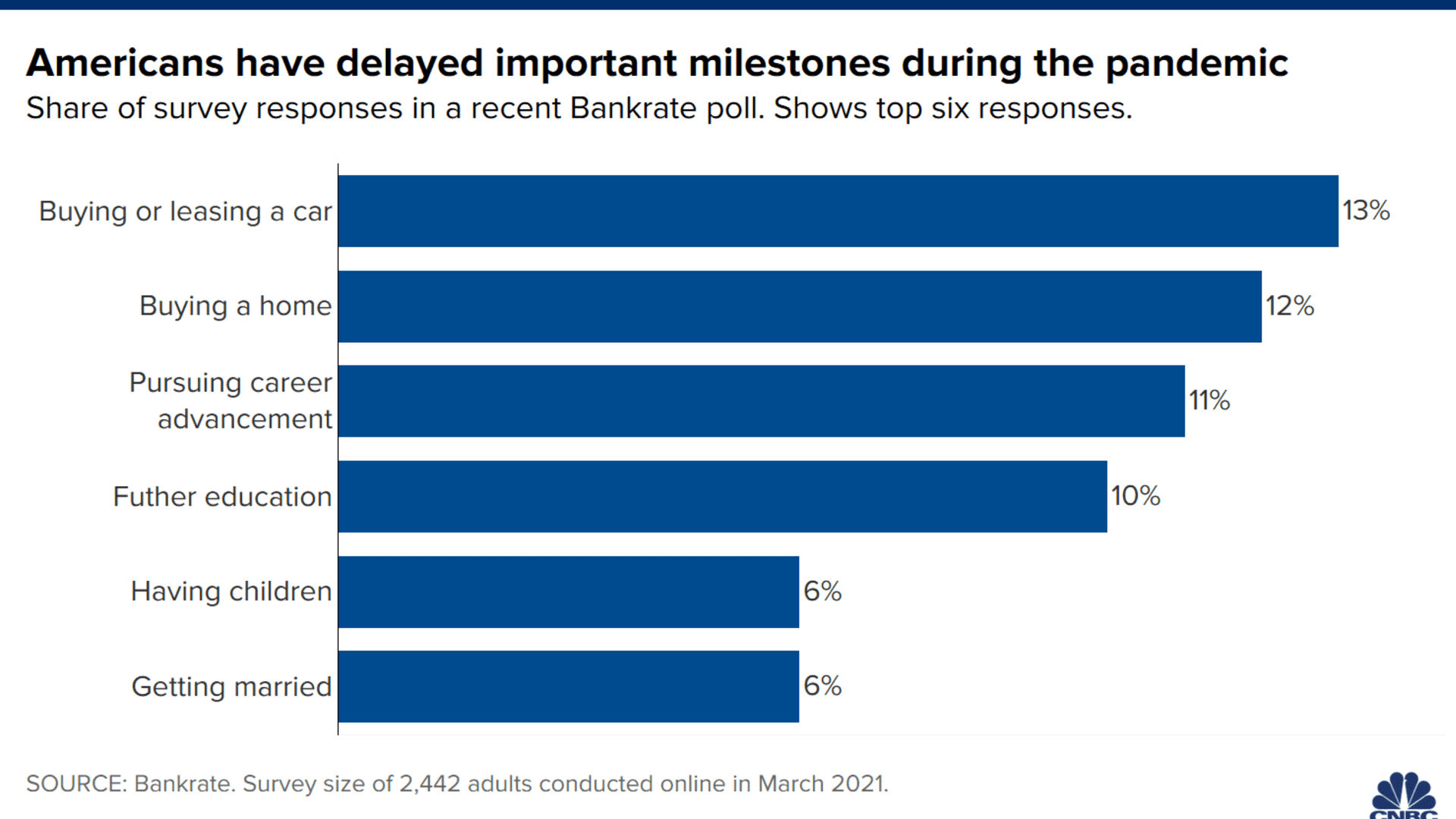

The most delayed financial benchmarks were buying or leasing a car, purchasing a home, pursuing career advancement and furthering education, according to Bankrate. Less popular milestones that were delayed included having children, getting married and retiring.

Money Report

"It stands to reason that those who tend to be more financially fragile are those who are earlier not only in their careers but in the complex aspects of their personal financial lives," said Mark Hamrick, senior economic analyst at Bankrate, adding that the youngest workers were also hardest hit by job loss during the pandemic.

The good news

Going forward, there is also some good news for those that were hit by Covid. As more people become vaccinated, the economy has been able to reopen more quickly than expected, getting more people back to work.

That may mean the road to a full recovery is closer than previously thought, according to Hamrick. As people return to work, they can begin to get back on track with their money goals.

Of course, that may be a long road for some, especially those that have had to take on debt to survive the past year.

"There's still going to be individuals that are going to be clawing out of this for quite some time," said Hamrick.

More from Invest in You:

How much to expect to get from Social Security if you make $40,000

'Catch Me If You Can' con artist says this scam is making a comeback

Prevent tax return anxiety by following these steps

It's important for those that have been hurt by the pandemic to remember they do have time to rebuild and that it doesn't need to happen overnight. The pandemic was an unforeseen event that few were prepared to weather.

"In some seasons, the greatest victory is enduring," said Tania Brown, a certified financial planner and coach at SaverLife, a nonprofit focused on helping low-income Americans save. "It's okay if you weren't able to meet some of your goals – your primary goal is to live, and secondary to that is reaching other goals."

How to rebuild

If you've had to delay a financial milestone because of the pandemic, it's best to take account of where you are before jumping back into rebuilding.

Before recommitting to financial goals such as buying a house or car, first make sure you've built up emergency savings and paid down debt, starting with high-interest debt first, Brown explained.

She recommends that people think about emergency savings in two ways – the first is to have a smaller emergency account that acts as a cushion for expenses you can't necessarily plan for, such as your car breaking down.

The second level of emergency savings comes after you've paid down your debt and are current on all bills. Then, you should aim to have three to six months of living expenses put away, according to Brown.

It's a good time to take stock of the last year and assess savings goals for many. The third stimulus check has hit bank accounts for most eligible Americans, sending them an extra $1,400 to spend or save.

In addition, it's also tax season, meaning many Americans will have a refund coming soon. So far, the average refund is $2,893, per IRS data.

If you've just received a stimulus check or refund, Brown recommends taking a small amount – say, 5% -- to treat yourself after a rough year. Then, the rest can be redirected to getting back on track with your financial goals.

"A treat with boundaries," she said.

SIGN UP: Money 101 is an 8-week learning course to financial freedom, delivered weekly to your inbox.

CHECK OUT: How to make money with creative side hustles, from people who earn thousands on sites like Etsy and Twitch via Grow with Acorns+CNBC.

Disclosure: NBCUniversal and Comcast Ventures are investors in Acorns.