- JPMorgan's Chase Bank will double its Chase Homebuyer Grant in an effort to foster homeownership among Black and Latino communities.

- Qualified homebuyers across the country can now receive a $5,000 grant when purchasing a home through the bank.

- "I daydreamed," said new homeowner Marcia Hernandez when asked about her grant. "It secured me from worrying in the future. I was shocked."

The early days of Guadalupe Mora's search for a new home were exhausting.

A health-care technician at a Department of Veterans Affairs hospital, Mora slowly saved up more than $15,000 to move out of her two-bedroom mobile home and into a new place she picked out with her real estate agent.

But the lender she had first contacted started to hound her day and night, pressing her with demands for even more cash and other proof she would be able to pay off a loan.

Get New England news, weather forecasts and entertainment stories to your inbox. Sign up for NECN newsletters.

A single mother to a 12-year-old who "thinks he knows it all," Mora said the lender's agents would harass her with messages even when she made it clear she could not return texts while at work.

"It was, seriously, so stressful. It was horrible," she told CNBC last week during her lunch break. "I work 12-hour shifts. I cannot — especially when I'm working in the Covid unit — it's impossible for me to be on my phone constantly."

The lender "just did not understand that I knew I needed the house — and I wanted the house. But I needed to keep my job in order to buy the house," she added.

Money Report

So, when Mora finally applied for a mortgage through Chase Bank, the 45-year-old learned she qualified for its $2,500 Homebuyer Grant, one of the bank's programs designed to help customers finance the purchase of a home.

The grant is just one of several assistance options U.S. banks have deployed in recent years to foster homeownership among Black and Latino communities that have historically faced higher hurdles when applying for a mortgage.

To further advance that goal, Chase Bank announced on Tuesday that it will double its Chase Homebuyer Grant.

Chase, the U.S. consumer and commercial banking business of JPMorgan Chase, said qualified homebuyers in predominantly Black neighborhoods across the country can now receive a $5,000 grant when purchasing a home through the bank.

While that sum may represent a fraction of the price of a home, it can help cover a substantial portion of an applicant's down payment or closing costs, often the largest hurdles for new homebuyers.

'Part of the solution'

Chase's move to boost the Homebuyer Grant comes just over four months after the bank pledged $30 billion to help address U.S. wealth inequality, especially in historically underserved Black and Latino communities.

The bank pledged to use the $30 billion to finance an additional 100,000 affordable housing units and write 40,000 new home-purchase loans for Black and Latino households.

Still, housing advocates say the bank programs are overdue after decades of redlining, the subprime mortgage crisis and risky high-interest loans to Americans with a short or tarnished credit history.

Many banks announced their new mortgage assistance programs in the months after the May 25 death of George Floyd at the hands of a police officer and weeks of Black Lives Matter protests across the country.

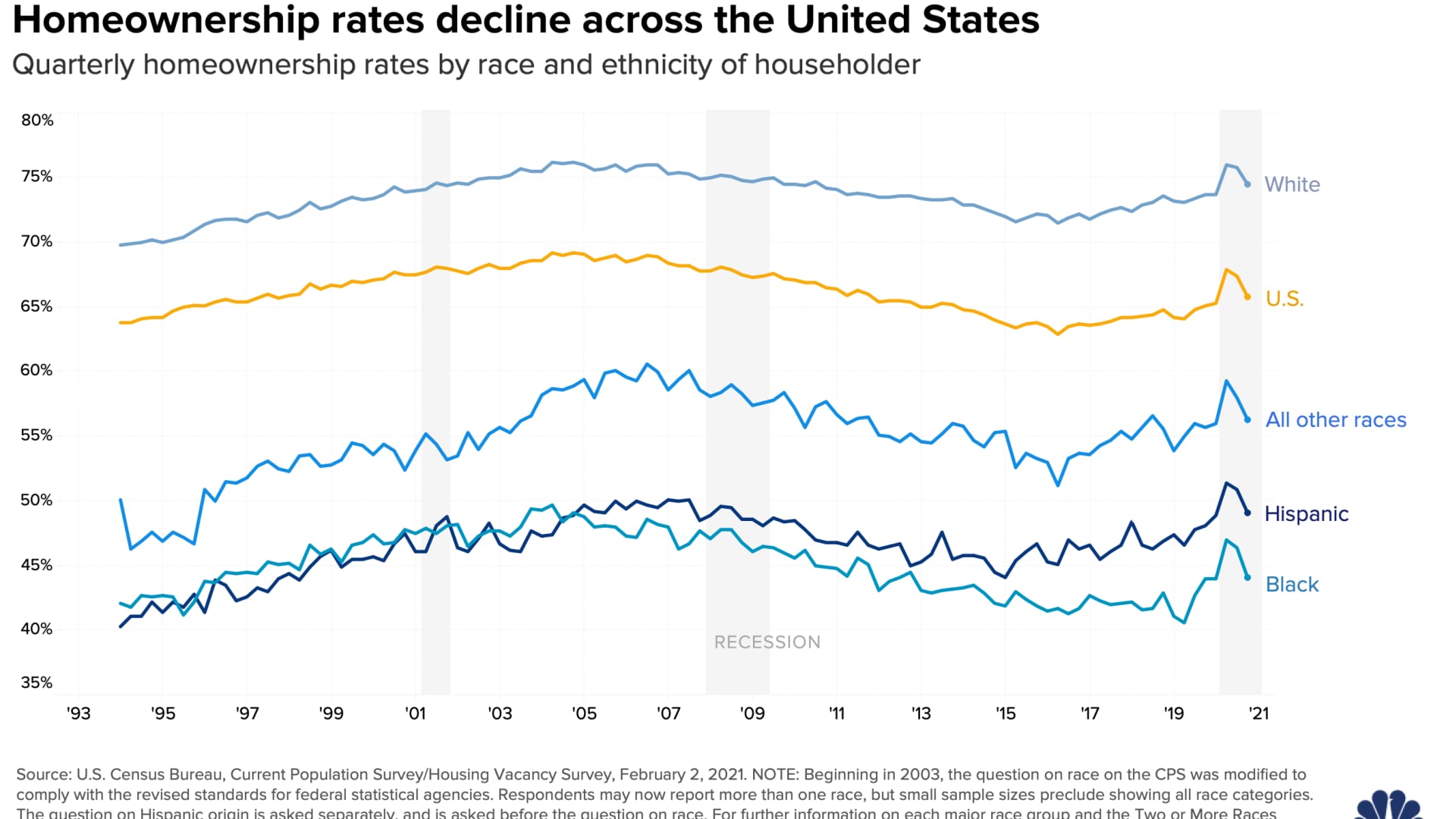

Black homeownership levels are especially low and have consistently trailed those of other minority groups and White households.

In the first quarter of 2020, 44% of Black families owned their home, compared with 73.7% of non-Hispanic White families, according to data from the Census Bureau. By the fourth quarter, that difference had widened slightly to 44.1% for Black families and 74.5% for White families.

Black households saw homeownership rates slump to 40.6% in 2019, the lowest level for the demographic going back through Census data dated 1994.

Though Black homeownership has recovered somewhat since then, the impact of Covid-19 and the subsequent recession kept downward pressure on the rate of Black homeownership throughout 2020.

Cerita Battles, head of the Chase community and affordable lending team, told CNBC she believes lenders need to play a proactive role in working to reduce those disparities.

"Absolutely yes. We should be a part of the solution," Battles said Thursday.

"I think about myself, being someone that is Black," she continued. "There were times when I bought my first home — I couldn't go to my parents and ask them for dollars to support me in my down payment. And I didn't have a whole lot of wealth to begin with because of the different jobs that I had, and how I had to come up."

Battles said she and her husband, who is a veteran, received a significant portion of the funds to purchase their first home through a loan backed by the Department of Veterans Affairs. Banks often offer more favorable lending terms to applicants who qualify for a VA loan since the department guarantees a portion of the mortgage.

Similar initiatives are underway at Bank of America, which announced on Feb. 3 that it would invest $15 billion in affordable housing programs over the next five years, tripling its prior commitment.

Steve Boland, president of BofA's retail business, told CNBC at the time that demand for its initial $5 billion pledge was so robust that applicants had quickly exhausted the allotment.

"We see the need. We got great response from our clients. And so we thought it was appropriate to try to triple that and get that done to 60,000 homeowners by 2025," he said.

Rebuilding trust

Though the industry has received praise for its attempts to prioritize homeownership among minority communities, the programs come after years of criticism from advocacy groups that say big banks for decades worsened racial discrimination in the U.S. housing market.

Codified racial bias in the U.S. housing market dates back nearly a century, when government officials openly engaged in a practice known as redlining.

Starting around the 1930s, surveyors would outline and grade neighborhoods in hundreds of U.S. cities to determine which were safe enough to finance. Communities that included more people of color were more often deemed credit risks and, by extension, denied a variety of financial services, including mortgages.

Though Congress outlawed redlining in the 1960s, recent housing research shows that the uneasy relationship between the Black community and the lending industry was fraught well into the 21st century.

In the early 2000s, Black households were disproportionately targeted with dicey subprime loans, leading to the foreclosure of more than 240,000 homes owned by Black people and a foreclosure rate nearly double that of White people.

In a 2016 complaint, the U.S. Consumer Financial Protection Bureau alleged that BancorpSouth unlawfully denied Memphis-area Black applicants certain mortgage loans and overcharged some of its Black customers.

The complaint asserted that the bank required its employees to review applications from minorities more quickly than others, and not to provide them the opportunity to receive credit assistance that might have improved their chances of getting a loan.

A more recent study from the University of California at Berkeley found that Black and Latino applicants continue to face higher borrowing costs.

The 2019 study, which reviewed 7 million, 30-year mortgages, found that Latino and Black borrowers "pay 0.079% and 0.036% percentage points more in interest for home-purchase and refinance mortgages, respectively, because of discrimination."

Lenders contend that these differences reflect the fact that minorities generally have less cash on hand and lower credit scores. Critics argue the disparities represent historical and structural problems that banks ought to help solve.

Acknowledging that turbulent history, Battles said a key first step in correcting the homeownership statistics is to try to guarantee that Black and Latino communities are aware of the new financial services available to them.

"There are a lot of different things, I would say, that lenders can do to support this effort," Battles said. And that, she said, starts with building trust in each community.

"We have to make sure that we're hiring people that mirror the markets we're seeking to serve," she added. "It is important for us to make sure that we have folks that are out there that can cultivate relationships and win the trust and consideration of these customers and these communities."

Marcia Hernandez, just married in August, says her years of history as a Chase customer was key when she and her partner, Vivian, started looking for a new home in a quieter neighborhood in the Miami area.

"For years I have had Chase and I first started with my lending," she said. "I educated myself a little more online and I ended up submitting a prequalification and I got a call within the same day."

The 31-year-old says she worked with a home lending advisor at Chase to determine a reasonable budget and the resources available to her. Though Hernandez wasn't eligible for a grant initially, a representative for the bank said it recently told her she had been awarded its new $5,000 grant.

"I daydreamed," she said when asked about the grant. "It secured me from worrying in the future. I was shocked. I couldn't believe it."

"It opened room for other projects," she added.

Hernandez, scheduled to close on her house on Tuesday, said she's eager to repaint the walls and add plants to her new home.