- S&P 500 companies are surprising to the upside in earnings by 1.6%, the smallest magnitude in 15 years, according to Refinitiv.

- While some big consumer brands are still able to raise prices to defend margins, cost cuts are increasingly responsible for quarterly beats of Wall Street estimates.

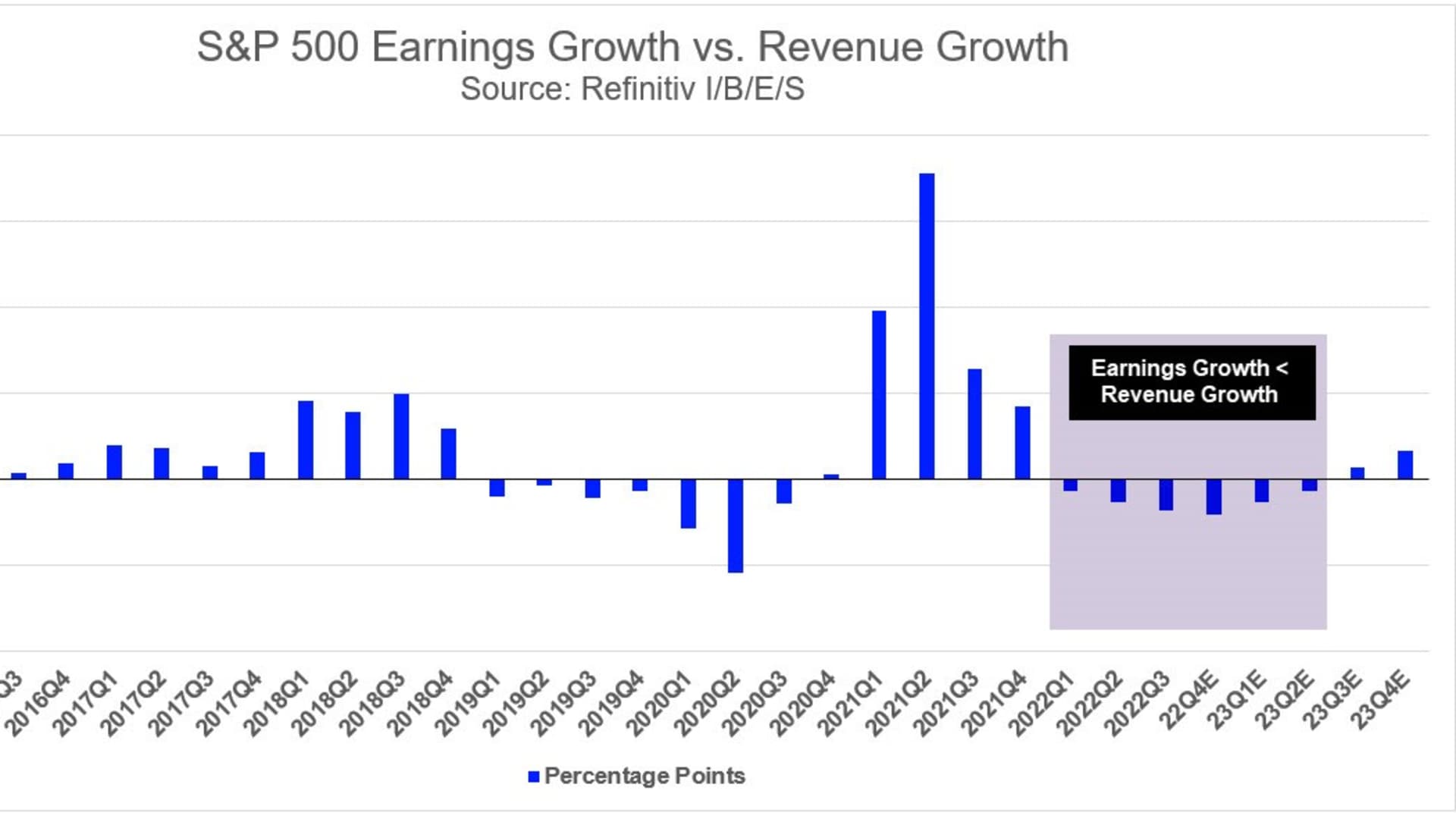

- The operating leverage that drove record profit margins earlier during the pandemic are becoming less common and more cost cuts will be needed across sectors of the economy.

Gone are the days when every company could just count on post-pandemic pent-up demand to drive results. Some industries are still benefiting from that, including airlines, hotels, casinos, credit card companies and some restaurants. And as companies seek ways to preserve margins and offset demand issues, price hikes are still an option, at least for companies focused on the core consumer basket.

Big brands have seen earnings propelled by double-digit price hikes – even if it has had a negative impact on demand elasticity. Just look at some of the companies that have raised prices but have seen volumes fall in the latest quarter:

- ConAgra: Prices up 17%, volumes down 8%

- Kraft Heinz: Prices up 15%, volumes down 5%

- Clorox: Prices up 14%, volumes down 10%

- Colgate-Palmolive: Prices up 13%, volumes down 4%

- Coca-Cola: Prices up 12%, volumes down 1%

- Procter & Gamble: Prices up 10%, volumes down 6%

Get New England news, weather forecasts and entertainment stories to your inbox. Sign up for NECN newsletters.

But the outlook is getting more cautious from consumer bellwethers. On Monday, both Walmart and Home Depot warned that they expect a tougher year ahead. And that caution arrived amid what's turning out to be the weakest earnings performance for S&P 500 companies since Q3 2020, with earnings falling 2.8% year-over-year so far this season. And when it comes to positive surprises, earnings have been a mere 1.6% above estimates, the smallest magnitude in 15 years, according to an analysis from Refinitiv's Tajinder Dhillon. Only two-thirds (67%) of the companies that have reported have beat earnings estimates, the lowest beat rate in eight years. And that is even after estimates were slashed in the weeks and months prior to earnings season — a meager beat rate even with a very much lowered bar.

With the latest view on the Fed being that it may not cut rates quite as soon as the market had hoped, recession clouds are back over the economy. That means preserving margins and profitability requires a closer look at spending – not just from the consumer, but from inside the corporation.

Money Report

Cost cuts are becoming increasingly important to help companies' bottom line. We saw this in the early days of the pandemic, when demand evaporated as economies around the world shut down. Companies got leaner. They got more efficient. They had to make some tough decisions. That's happening again amid waning demand and as companies plan for a potential recession.

One obvious way to cut costs is to reduce the workforce. We've seen many examples of this in recent weeks, headed into and during this earnings season, from Disney under activist pressure to the country's major banks to the tech sector layoffs that have topped the headlines. But workforce reductions aren't the only way for companies to cut costs, or necessarily the best way in a tight labor market.

From marketing costs to modifying capex plans, companies are finding ways to streamline operations and deliver better results to the street. We've seen notable examples across industries of just how important general cost cuts have been this earnings season.

Airbnb's EPS nearly doubled Wall Street expectations even with revenue was only slightly above estimates. Managing costs was key as the company hit some hurdles on both bookings as well as rates. Costs and expenses in the quarter rose 14%, far less than the 24% revenue growth which allowed for what the company described as "considerable margin expansion." Of course, Airbnb was one of the first companies to cut costs when the pandemic hit. Now it's becoming part of a permanent shift, according to the company's management: "We made many difficult choices to reduce our spending, making us a leaner and more focused company, and we've kept this discipline ever since."

Under Armour didn't have a stellar quarter for sales or gross margins. Retail store sales fell 6% and gross margin contracted 6.5 percentage points year over year and was nearly 1 percentage point below Wall Street estimates. But earnings beat estimates thanks to better cost management. The saving grace: operating margin comfortably exceeded consensus estimates as SG&A expenses dropped 11% year over year.

In retail, Ralph Lauren's results beat expectations even as revenue only grew 1% and gross margin was basically in line. Operating margin and the bottom line were helped by a 1% decline in operating expenses. Coach parent Tapestry saw lower North America sales, but the region's operating margin was better than the company had anticipated.

And there's the flip side to the story. Expedia blamed bad weather for a disappointing quarter, but the big issue wasn't a revenue decline. That was a tad short of Wall Street estimates, but earnings were a far bigger miss, 24% below consensus. Rising costs were a likely culprit for pressure on the company's bottom line. Sales & marketing expenses soared 32%, far outpacing the 15% revenue growth. That's problematic.

Michael Kors' parent Capri Holdings saw a 6% drop in revenue but a 7% increase in expenses – never a good sign. CEO John Idol also made it a point to tell investors and analysts, "We have begun taking measures to better align operating expenses with the change in revenue by channel."

In other words, they're going to have to do a better job managing costs.

What CFOs are saying about cost cuts

The cost-cutting message coming out of some notable earnings calls is more widespread. Approximately half of all companies (49%) are looking to reduce their spending to increase profitability, according to a new survey of CFOs and finance leaders from spend management software company Coupa.

"Clearly, the macro conditions are slowing, for technology for sure, but broadly for most companies and the other place to turn is cost," Tony Tiscornia, Coupa CFO and a member of the CNBC CFO Council, said of the balance between price hikes and cost cuts.

Under pressure to cut costs from investors and boards, headcount reduction is one place to look, but the Coupa survey finds that most CFOs are not turning to layoffs first, with more than 4 in 5 (86%) of CFOs and finance leaders saying they currently view this as a last resort; an almost equal number of respondents told Coupa they worry layoffs will result in longer-term labor issues.

Almost all CFOs surveyed (over 90%) are concerned about hitting sales forecasts in the year ahead and the risk of recession, with a little under half (42%) specifically concerned about maintaining profitability and margins.

"All the CFOs I speak with, and meet, are preparing for turbulence," Tiscornia said. Rates are up and growth is down, but the job market remains tight. "People are saying whether we're in a recession or not, I need to figure out how to batten down the hatches."

To drive growth in the event of a recession, a significant percentage of companies (38%) tell Coupa they still see room to increase prices. But roughly one-third of companies are looking more closely at the cost side. One-third (33%) expect enforcement of stricter rules on spending and expense limits to be the growth driver in a downturn, while 32% cite reduced business travel, though Tiscornia noted a lot of the low-hanging fruit in travel was already cut during the pandemic. Real estate is another area of ongoing focus, Tiscornia said, as leases and subleases come upon termination dates and companies have a better sense for their permanent post-Covid work approach.

CNBC surveying of CFOs has shown the majority to be in the "hard landing" camp for the economy. Tiscornia says that view comes with the duties of being a risk-focused CFO. "Expect the worst, plan for the worst, and hope for the best. That's our job and we need to set expectations. … For the most part, growth has come down and across most industries, at least the growth percentage," he said.

Coming from a tech sector view of the world, Tiscornia noted the role of the big shift that has taken place among investors. They've transitioned from years of placing the primary weighting on growth over cash flow or profitability, which had been roughly 85/15, to now being 50/50.

Across the economy, mission critical systems will be prioritized over new implementations. That doesn't mean IT spending goes negative, Tiscornia said, but it will decelerate. And that means the focus from vendors will also turn to cost management and tilt away from price increases.

Tiscornia says battening down the hatches means that CFOs "want to make smart investment decisions and put in the infrastructure 'I can afford' and which has a quick ROI for automation and controls for the next two to three years."