- The bond market had a wild ride on Thursday, reacting to the Fed’s willingness to permit the economy and inflation to run hot as the job market recovers.

- Strategists say that the market had initially responded to the Fed's dovishness and forecast for no rate hikes through 2023.

- By Thursday morning, rising inflation was the top concern. The bond market reacted dramatically to the Fed's policy to allow it to run above its 2% target.

Treasury yields flared on Thursday as bond market players grappled with the Federal Reserve's willingness to allow inflation to heat up.

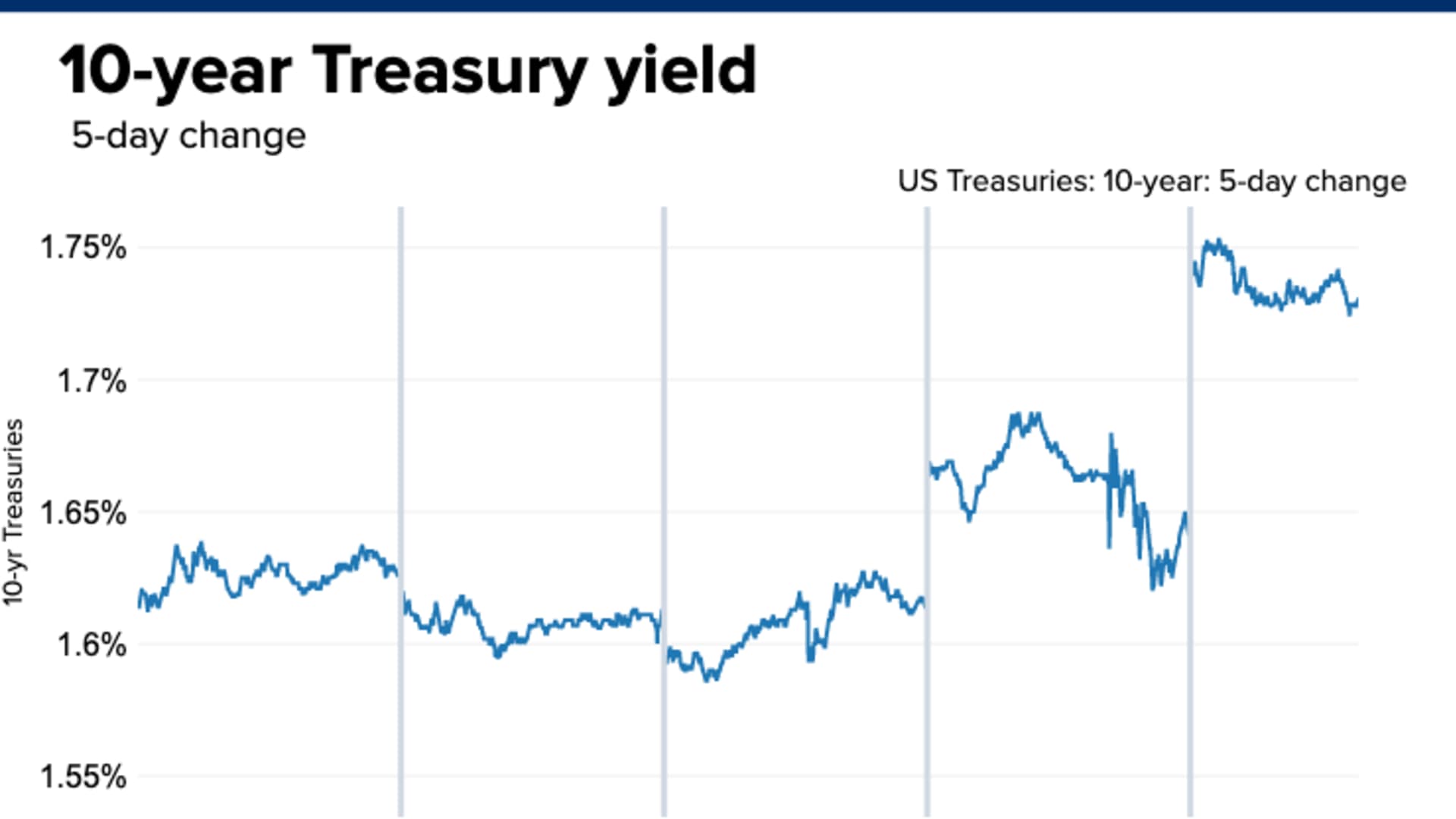

The 10-year Treasury yield shot up from 1.64% late Wednesday to 1.75% Thursday, a 14-month high. It was at 1.706% in afternoon trading.

The rise in yields – which move opposite to price – comes a day after Fed Chairman Jerome Powell reassured the market that the central bank isn't ready to dial back its bond purchases and other supportive measures.

While bond market pros say there was no development that kicked off the spike in yields on Thursday, the market's focus seems to have turned to the fact that the Fed plans to let inflation run hot.

"I think this is the bond market coming to terms with the fact that inflation might be happening and it might be coming because the Fed is assuring us they can live with inflation," Sonal Desai, chief investment officer at Franklin Templeton Fixed Income Group, told CNBC.

Money Report

A steeper yield curve

The run-up in interest rates, for now, does not pose a risk for the economy. Strategists say the yield is still relatively low, particularly given the expectation for explosive economic growth this year.

However, the move in yields overnight was especially large, even given the recent increase in the 10-year yield, which was at 1.07% six weeks ago. The benchmark 10-year is widely watched, as it influences mortgage rates and other consumer and business loans.

The bond market barely moved Wednesday afternoon, after the Fed issued its 2 p.m. ET statement and after Powell briefed the media.

Desai noted the effect of the market's reaction will be a steeper yield curve, which simply means a larger spread between yields of different maturities, like the 2-year Treasury notes versus the 10-year.

A steeper curve is often seen as a positive sign for growth, while a flattening curve can be a warning.

Ralph Axel, U.S. rates strategist at Bank of America, said the market on Wednesday was responding to one part of the Fed's statement, which sent a mixed message.

"The first message that sort of surprised people was that 'we don't believe in hikes in 2023,'" he said. "I think that was where the initial focus was, and I think that kept the dampening down on the initial reaction."

The second message was the Fed was going to hold rates down, let the economy run hot and allow inflation to increase, to help recover lost jobs, Axel said.

Interpreting the Fed's message on inflation

The market was directly responding to the Fed's policy of allowing inflation to now run in an average range around its 2% target.

"The market is grappling with what does that [average inflation targeting] mean in practice," Axel said. "We're coming to understand it means higher growth and higher inflation in the longer run, which means higher interest rates."

"When the Fed used to get a whiff of inflation pressure, the Fed would start tightening in on that," he added. They would cut off the recoveries a little early."

The idea was to prevent periods of booms and busts by cutting off the potential for deeper recessions as well. However, the Fed is now facing an economy that could boom, and with very high economic growth could come inflation, Bank of America's Axel said.

Second quarter growth is expected to be over 9%, according to the CNBC/Moody's Analytics Rapid Update.

Inflation is still low, with the core consumer price index, excluding food and energy, at annual rate of 1.3% in February. However, starting this month inflation levels could tick up due to the base effect from last year's big decline in prices during the economic shutdown.

The market has been challenging the Fed by pricing in rate hikes for 2023. Meanwhile, the central bank's collective forecast, called the dot plot, shows no consensus for a rate hike through 2023.

Managing Treasury supply

Tony Crescenzi, portfolio manager and market strategist at Pimco, said the market is also pricing in the fact that the Treasury will have to issue a lot of supply to pay for fiscal stimulus, given the most recent $1.9 trillion package and prior pandemic programs.

"A lot of what's happened in the pricing in of Treasury supply and the ability of market participants to absorb that supply, and this inflation fear," he said. "Part of it could be a head fake, but no one really knows so market participants have to price in the possibility that inflation could accelerate beyond what is expected."

Market expectations are for inflation to average about 2.30% over the next 10 years.

"So long as the overall financial conditions remain conducive towards a strengthening in economic activity, then the Fed need not worry about the rise in interest rates to this point," Crescenzi said.

Choppiness in the stock market as yields rise

So far, the stock market has reacted to the rate rise with choppy moves up and down. On Thursday, stocks were lower after Wednesday's rally, and the tech-heavy Nasdaq Composite was particularly hard hit.

"I wouldn't be shocked if we had a bigger pullback in the stock market if this thing [10-year yield] goes to 2% quickly," said James Paulsen, chief investment strategist at The Leuthold Group.

He said the stock market would be concerned if the pace of the interest rate move remains rapid, but if it is able to adjust to the increases gradually it would not be a problem.

"If you're going to have a year where rates go up, it couldn't be a better year," Paulsen said, noting economic growth could be 8%. "I think it's a pretty good year for this to happen to the economy and stock market. Their vulnerability isn't nearly as great as they could be further down the road."

Paulsen expects the 10-year yield to reach 2% by year end.

Crescenzi said since the level of the 10-year yield is partly based on inflation expectations, it has had to adjust to the Fed's use of the average target range, instead of a set target.

"By indicating it will delay its rate hike until inflation picks up and employment goes back to maximum employment, the anchor for inflation expectations is not as strong," he said, "That's what's letting the inflation component in the rise in yields become unleashed, to an extent."

Crescenzi said the dovishness of the Fed Wednesday may be a sign of a new view from the central bank.

"It does seem to suggest the Fed is taking a more holistic view of financial conditions, as Powell pointed out by citing the financial conditions as a whole, instead of honing in on yields by themselves," he said.