- The Federal Reserve on Wednesday said it would keep its benchmark interest rate near zero.

- There are a few ways consumers can still take advantage of the low-interest rate environment while it lasts.

The Federal Reserve said Wednesday it will keep its benchmark interest rate near zero to continue to support the economic recovery from the coronavirus pandemic.

It's been over a year since the central bank slashed its benchmark overnight lending rate. The Fed also instituted a series of programs to keep credit flowing when the pandemic shut down the economy.

Now the economy is gaining steam, bolstered by fiscal and economic policy, as well as the growing numbers of people vaccinated against Covid-19.

Get New England news, weather forecasts and entertainment stories to your inbox. Sign up for NECN newsletters.

But with millions of people still out of work and cash-strapped, the Fed said it is sticking with its policies for now.

"Economic growth is kicking into higher gear, but with 6% unemployment, an uneven household recovery and more than 2 million fewer Americans in the labor force than prior to the outbreak, the Fed is keeping the throttle wide open," said Greg McBride, chief financial analyst at Bankrate.com.

Money Report

More from Personal Finance:

Worried about inflation? This investment may be for you

Many households may pay zero in income taxes this year

Those $1,400 stimulus checks are still arriving by mail

Although the federal funds rate, which is what banks charge one another for short-term borrowing, is not the rate that consumers pay, the Fed's moves still affect the borrowing and saving rates they see every day.

The Fed's historically low borrowing rates has made it easier to borrow money — while also making it less desirable to hoard cash.

Here's how consumers can take advantage of the Fed's near-zero rate policy while it lasts.

Refinance a mortgage

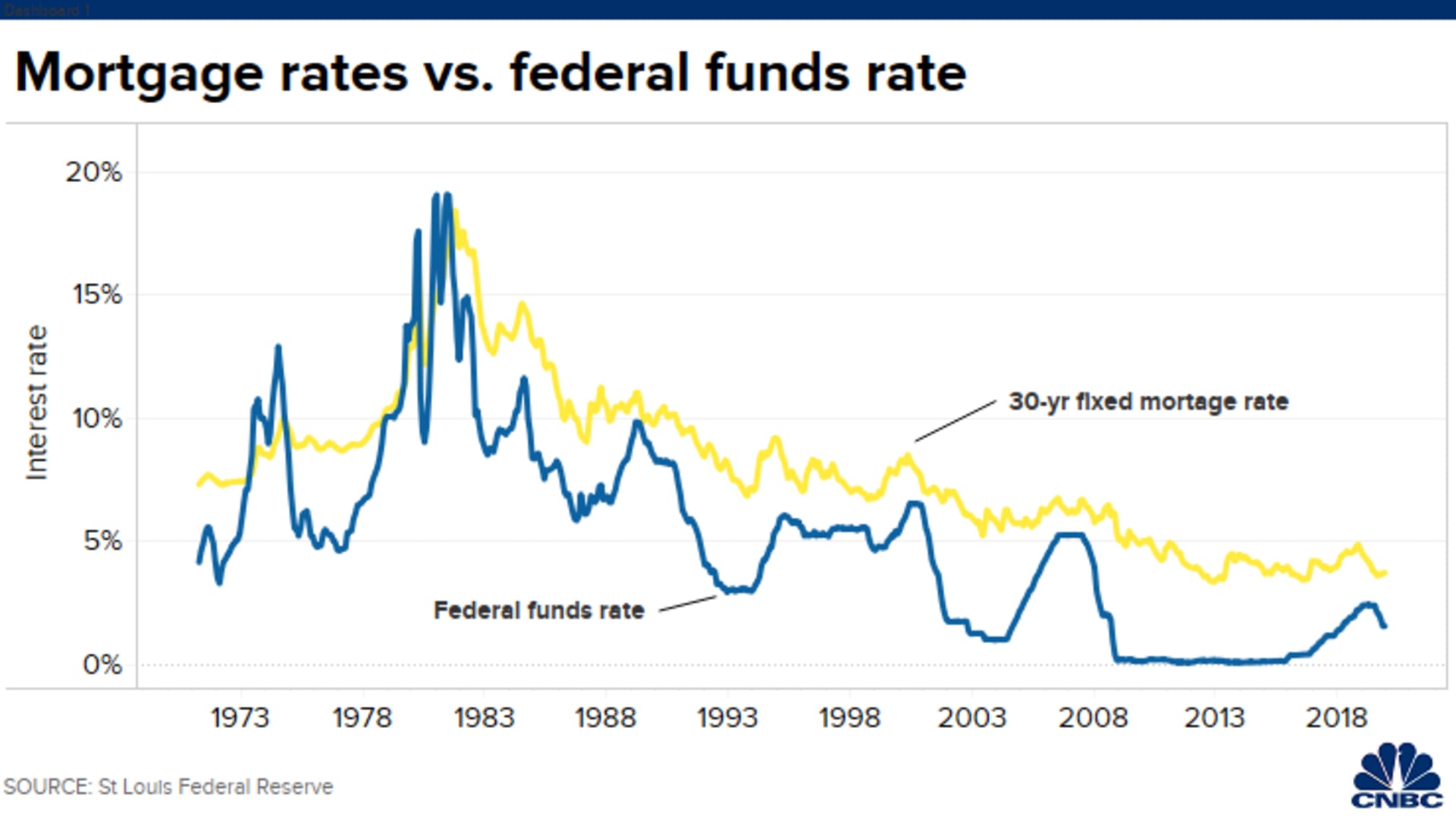

The economy, the Fed and inflation all have some influence over long-term fixed mortgage rates, which generally are pegged to yields on U.S. Treasury notes.

Currently, the average 30-year fixed-rate home mortgage is 3.21%, up slightly from its record low, according to Bankrate.

"The Fed drove mortgage rates lower in 2020," said Tendayi Kapfidze, chief economist at LendingTree, an online loan marketplace. Although rates are now rising, they are still low enough to support the housing market, he added.

"if you haven't yet refinanced, there is still time to do so," McBride said.

Consumers can save themselves money if they refinance existing debt for a lower rate. In fact, this may be the best way to free up cash, McBride said.

Pay down debt

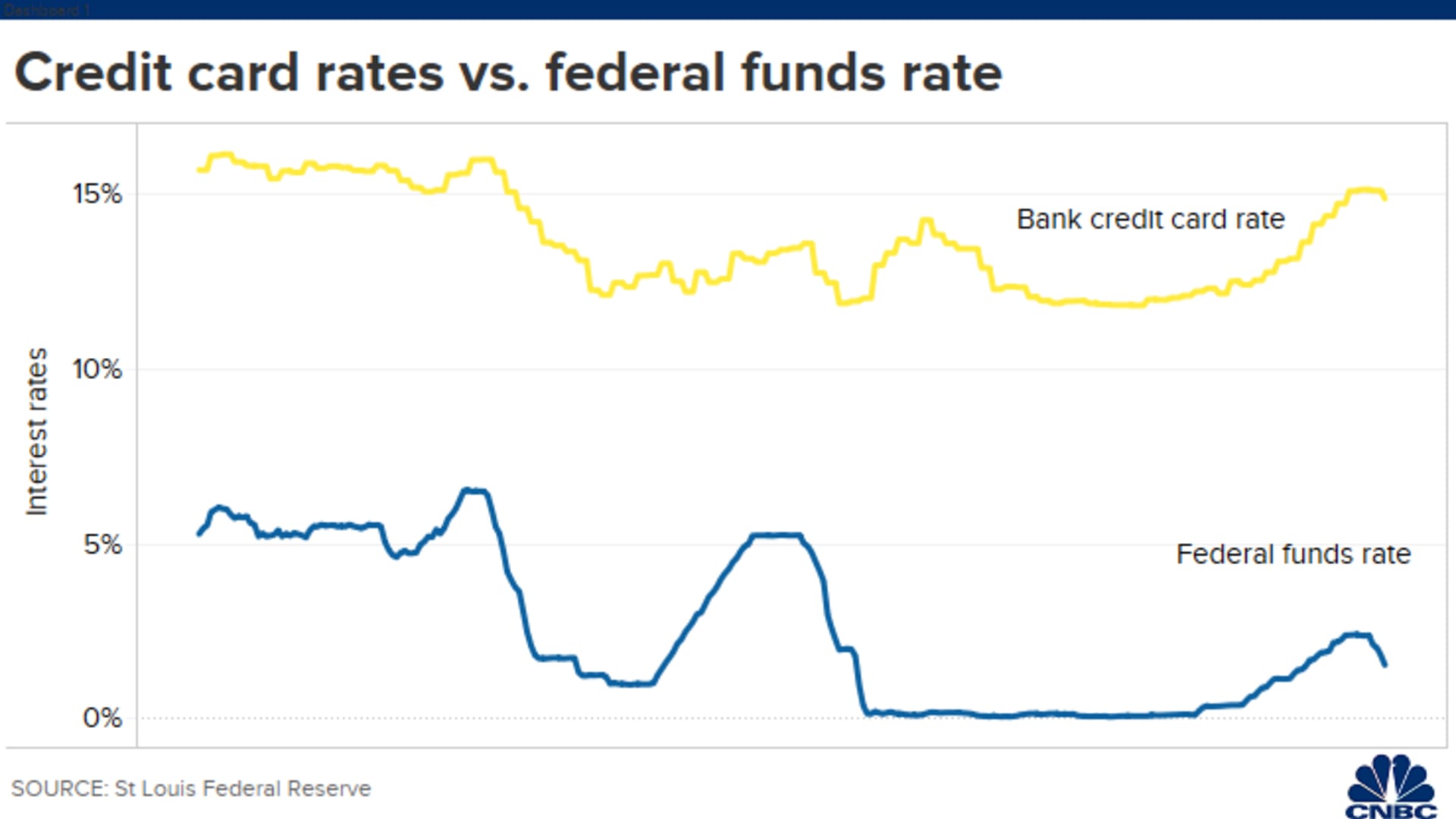

Most credit cards come with a variable rate, which means there's a direct connection to the Fed's benchmark rate.

Since the central bank moved its benchmark rate to near zero in last year, credit card rates have hit a low of just under 16%, on average, according to Bankrate.com.

Still, other short-term borrowing rates are now even lower. "Consider switching to a lower-cost loan, such as using a personal loan to consolidate and pay off high-interest credit cards," Kapfidze advised.

"You may significantly lower your overall debt costs."

For those struggling with college debt, this is a great time to stay up-to-date on payments even though the CARES Act paused federal student loan repayment through September, McBride said.

While interest is suspended, "every dollar will go toward reducing the balance."

Boost emergency savings

To be sure, low interest rates aren't good for everyone, particularly savers. However, the government's Covid relief payments provide a rare chance to shore up your financial standing.

"Between stimulus payments and tax refunds, it's a great opportunity to make some significant headway on your emergency cushion," McBride said.

"One of the best things Americans can do right now is build up their savings while trimming their debt," said Matt Schulz, chief credit analyst for LendingTree.

"That savings is the best way to ensure that you don't just get right back into the cycle of debt after paying off your credit card."

Although the Fed has no direct influence on deposit rates, those tend to be correlated to changes in the target federal funds rate, and, as a result, savers are earning next to nothing on their cash.

The average savings account rate is a mere 0.06%, or even less, at some of the largest retail banks, according to the Federal Deposit Insurance Corp.

But thanks, in part, to lower overhead expenses, the average online savings account rate is at least three times higher than the average rate from a traditional, brick-and-mortar bank.

"Online savings accounts still remain a solid option for short-term savings and emergency funds," said Ken Tumin, founder of DepositAccounts.com.

In fact, the pandemic has even given digital banks a boost, resulting in more competition to offer better rates.